IPC Private Wealth - IPCC Corporate

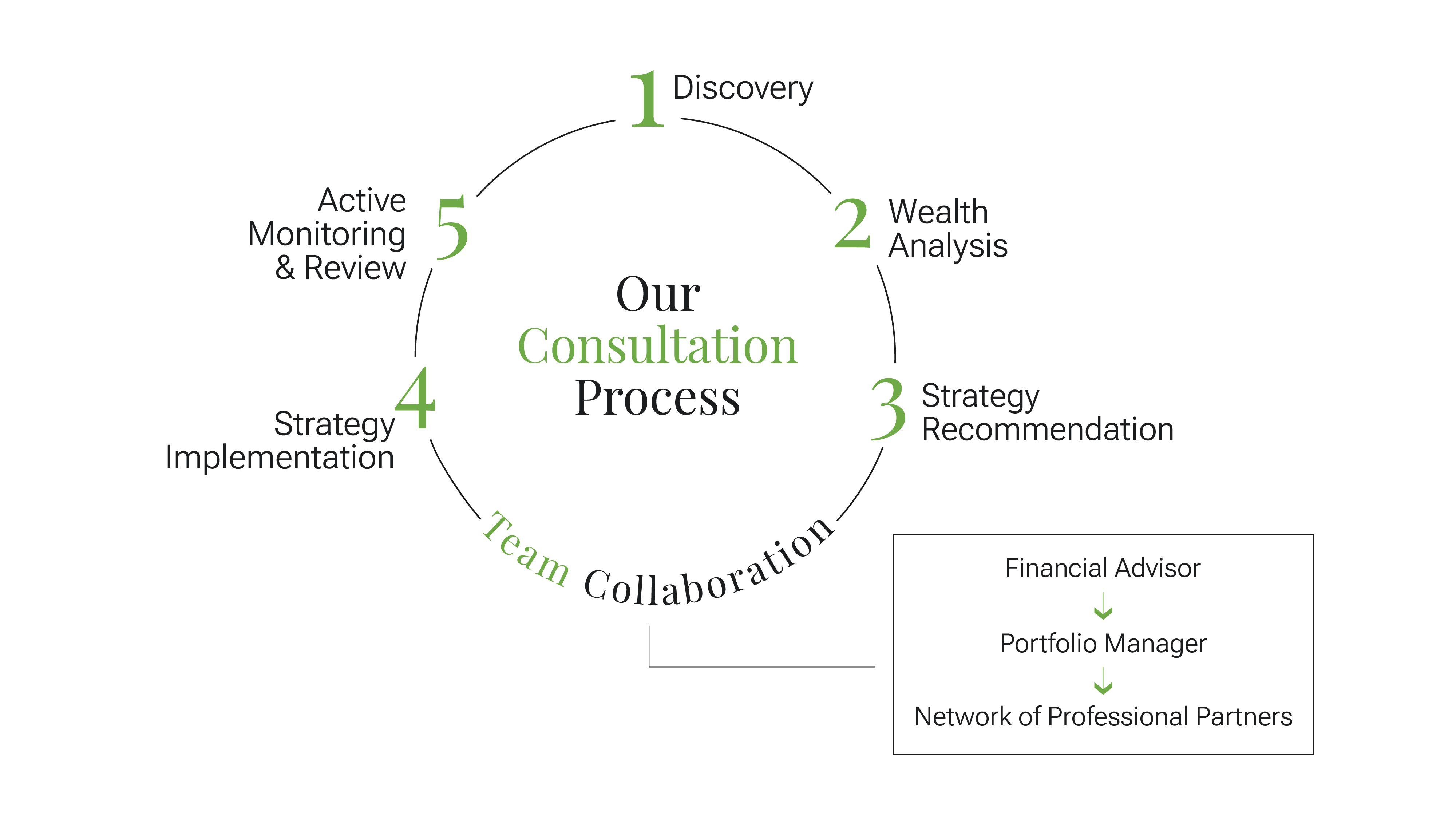

Understanding First

We begin by listening to learn what’s important to you, understand your priorities, and uncovering potential risks. We use this knowledge to tailor your investment strategy with wealth-enhancing solutions that target your precise needs and opportunities.

An Integrated Approach for Better Outcomes

Our dedicated Portfolio Managers will consult with your Advisor, and a network of financial experts at every stage of the process and consider every element of your wealth strategy.

Based on your needs, we’ll integrate the right combination of investment and tax strategies to meet your cash flow requirements, efficiently grow, protect and transition your wealth, and give back to your preferred charities. Through thoughtful planning and continuous reviews, we'll bring you advice and coordinated strategies that lead to better long-term outcomes for you and your family.

We’ll manage your financial risks and take advantage of opportunities to preserve your wealth and protect your legacy.